Introduction

This time last year, it was well understood that 2024 would be a year dominated by pivotal elections across the globe, including key contests in India, Mexico, South Africa, the US and the UK. Many of these elections saw incumbents losing power, their majority, or significant voter share. However, the most unexpected outcome came from the US, with the victory of Donald Trump. He will now make a historic return to the White House in January 2025.

From our perspective, this result took many, including those in the markets, by surprise. Going into the last few weeks of the election, the race was viewed as a close 50/50 contest. However, the prediction markets were leaning toward a Trump victory, which ultimately proved correct. What few anticipated was the Republican Party’s clean sweep across all branches of government as it captured the White House and the House of Representatives and regained the Senate. This outcome grants the Trump administration free rein to implement its policies with minimal opposition. In practical terms, this means swift confirmation of key appointments and the potential for decisive action on legislative priorities during the first Congressional session.

Markets have already reacted to this evolving political environment, reflecting a heightened risk premium tied to what some are calling the “Trump trade”. This has unfolded against the backdrop of an ongoing interest rate easing cycle, with the Federal Reserve (Fed) implementing a notable 50-basis-point (bp) rate cut in September and easing by a further 25 bps after the election. Despite initial market optimism following the Republican sweep, bond yields remain elevated as investors price in the uncertainty around Trump’s policy proposals.

Key policy and market impacts

While tariffs were a cornerstone of Trump’s first term, we expect them to remain a strategic negotiation tool rather than a broad-based revenue generator. His past actions suggest he will use the threat of tariffs to extract concessions rather than disrupt global trade entirely. For instance, he applied tariffs on French wine during his first term, not as a long-term policy, but as leverage to initiate discussions with French leadership. Looking ahead, Trump is likely to implement more punitive tariffs on China while adopting a more measured approach with Europe, using trade policies to encourage favourable outcomes rather than resort to blunt protectionism. Importantly, we believe tariffs will serve his broader agenda to reshore US manufacturing, a move that may marginally influence prices but is unlikely to lead to a significant resurgence in inflation.

While tariffs may modestly extend inflation trends, we are not alarmist about their potential impact. Any inflationary pressure from tariffs pales in comparison to the global monetary policy shifts seen during the pandemic, when central banks expanded the global money supply by more than 10%. Those policy actions still reverberate today, contributing far more to inflation than any potential tariff measures likely to be introduced. As we move forward, the disinflationary trends seen in recent years are expected to persist, albeit with slight adjustments influenced by evolving fiscal and trade policies. We would note that US inflation fell from 2.1% to 1.9% in 2018 when Trump first enacted tariffs.

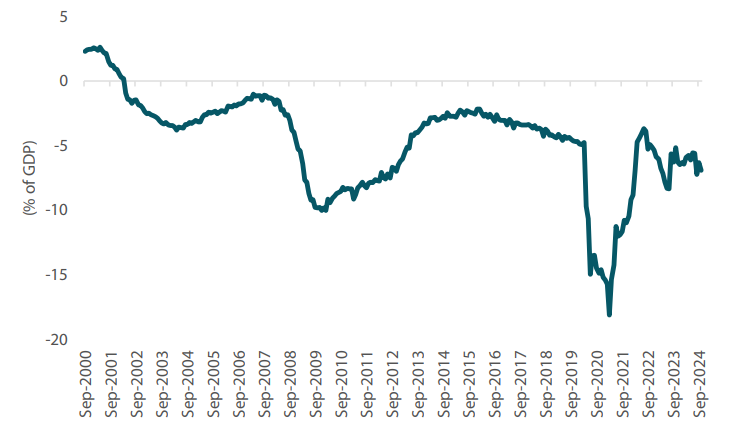

Another critical area to watch is the proposed extension of the Tax Cuts and Jobs Act (TCJA) of 2017. Trump’s stated goal is to make these tax cuts permanent, which could have significant implications for fiscal policy and the deficit. While the extension of the TCJA may provide a short-term boost to economic growth, there is broad recognition—both within Congress and among policymakers—that the US deficit, currently at 7% of gross domestic product (GDP), is unsustainable. Therefore, we think rationality will likely prevail, and any tax policy changes will aim to minimise long-term fiscal risks. This could mean deficit-neutral tax reforms or more targeted measures to balance economic growth with fiscal responsibility.

Chart 1: US Treasury federal budget deficit

Source: Nikko AM, Bloomberg as at 31 October 2024

Is Fed independence under threat?

The Fed’s role as an independent body has long been a cornerstone of effective monetary policy, providing a counterbalance to political influences. However, questions around this independence are becoming increasingly relevant, particularly as we look to 2025 and beyond. With Jerome Powell’s term as Fed Chair set to end in May 2026, speculation about his successor is already building. In a recent press conference, Powell made it clear he would not step down if pressured, reaffirming his commitment to Fed independence. Nonetheless, potential efforts by the Trump administration to reduce this independence, possibly through the appointment of a loyalist as the next Fed Chair, could introduce significant uncertainty for markets. Such a move would likely be viewed unfavourably by investors, given the critical role of political independence in ensuring balanced monetary policy.

While political considerations might shape who is appointed as the next Fed Chair, we believe the broader trajectory of monetary policy will remain largely unchanged. We expect the Fed will stay on its current easing path, as economic conditions, rather than presidential influence, continue to dictate its decisions. For example, there are growing signs of US labour market softness, despite official metrics suggesting strength. We believe the labour market is weaker than headline numbers indicate, supporting the case for less restrictive monetary policy. Coupled with our outlook for US inflation to moderate further, potentially reaching the sub 2% range in early 2025, there is a clear argument for continued rate cuts in the US.

European outlook: Germany at a turning point

Often seen as the economic engine of Europe, Germany has faced persistent challenges with sluggish growth (Chart 2), and this has contributed to broader difficulties across the European region. As we look ahead, a snap election scheduled for February 2025 may mark a turning point, introducing the potential for significant economic reforms and renewed momentum.

One of the central issues hampering growth in Germany has been the “debt brake”, a constitutional measure that limits government borrowing and prevents deficit spending. While originally intended to promote fiscal discipline, this constraint has restricted the government’s ability to invest in critical areas like infrastructure, particularly during economic downturns. Moreover, efforts to temporarily suspend the debt brake under “emergency provisions” citing factors like the war in Ukraine and the broader economic slowdown have faced legal and political hurdles. The refusal by Germany’s former finance minister to enact such a suspension ultimately led to his dismissal and the collapse of the ruling coalition, setting the stage for February’s election. The outcome of this election could pave the way for much-needed reforms. A new coalition government, potentially led by the centre-right Christian Democratic Union and a centre-left partner, may work toward either amending the debt brake or implementing emergency measures to enable greater fiscal flexibility. Such changes would open the door for increased investment in infrastructure and other growth-stimulating initiatives, both of which are critical for reviving Germany’s economic dynamism.

Chart 2: Germany’s industrial slump

Source: Nikko AM, Bloomberg as at 31 October 2024

Implications for broader European growth

Of course, a revitalised German economy would have positive ripple effects across Europe.

If new policies succeed in restoring Germany’s growth potential, the broader European economy could also see benefits, strengthening investor confidence in the region. From a fixed income perspective, this could have significant implications for European bond markets. Currently, European bonds have outperformed US Treasuries, supported by a relative macroeconomic advantage. However, a shift in Germany’s growth trajectory could alter the outlook for European yields. This could potentially lead to upward pressure on yields as markets adjust to stronger economic fundamentals.

UK and Europe: still in need of central bank support

Europe’s economic performance remains underwhelming, with structural issues like energy dependence and weak manufacturing growth weighing on the region. However, there are some signs of stabilisation. As mentioned, Germany’s sluggish performance has been a drag on the Eurozone, but potential fiscal reforms and infrastructure investments following February’s snap election could revitalise growth. Inflation is declining across Europe, and the European Central Bank (ECB) is likely to continue easing, with one more 25 bps rate cut expected in December 2024 and then potential rate cuts of up to 100 bps in 2025. The ongoing easing of monetary policy, in an environment of weak growth and easing price pressures, offers a modestly positive outlook for European fixed income markets.

The UK economy continues to struggle with weak growth, a depressed housing market, and elevated underlying inflation. Recent tax increases, including a hike in National Insurance paid by employers, may have the knock-on effect of suppressing wage growth and productivity further. The Bank of England is expected to reduce rates gradually, with markets pricing in limited cuts. However, we see potential for more aggressive easing, especially if economic conditions deteriorate further. Lower mortgage rates could provide a much-needed boost to the housing market and broader economic activity.

Commodity-exporting nations face challenges, but offer areas of opportunity

The economies of Canada and New Zealand are both experiencing subdued consumption due to elevated floating mortgage rates, which have rapidly transmitted tighter financial conditions. However, rate cuts are beginning to provide relief, and we anticipate gradual economic recovery driven by improved household finances and lower interest burdens. The Australian economy has shown greater resilience, benefiting from strong labour markets and government measures to offset cost-of-living pressures. However, inflation remains sticky, prompting a cautious approach from the Reserve Bank of Australia (RBA). While rate cuts are likely in 2025, the timing remains uncertain, with consensus pointing to easing by the RBA in Q1.

One to watch: Norway

Norway has emerged as one of the outliers in the global monetary policy landscape. While most major central banks are transitioning toward easing cycles, Norges Bank has maintained a particularly hawkish stance, holding policy rates steady despite tepid economic activity. The decision to keep rates elevated seems driven more by concerns about currency weakness than domestic economic fundamentals. The Norwegian krone has been one of the weakest-performing G10 currencies, which is a surprising trend given Norway’s robust fundamentals. Norway benefits from low public debt, a healthy fiscal surplus and the strength of its offshore oil-producing sector. And while the consumer sector has shown some softness, it is not the primary driver of the central bank’s policy decisions. Instead, Norges Bank has been explicit in linking its policy stance to currency performance, viewing a weak krone as a potential inflationary risk. This currency-driven approach explains why the central bank reversed a pause in rate hikes earlier in the cycle and remains cautious about reducing rates too soon.

The central bank has signalled it will maintain current rates through the end of 2024, with a revision to its outlook expected in December. While a rate cut is anticipated in 2025, the timing remains uncertain. Norges Bank’s approach makes it one of the last G10 central banks likely to initiate policy reductions. For the krone to recover, a stronger performance in the currency market will likely be needed. However, with such solid underlying economic fundamentals, any sustained weakness in the currency may present an anomaly rather than a reflection of Norway’s broader economic health.

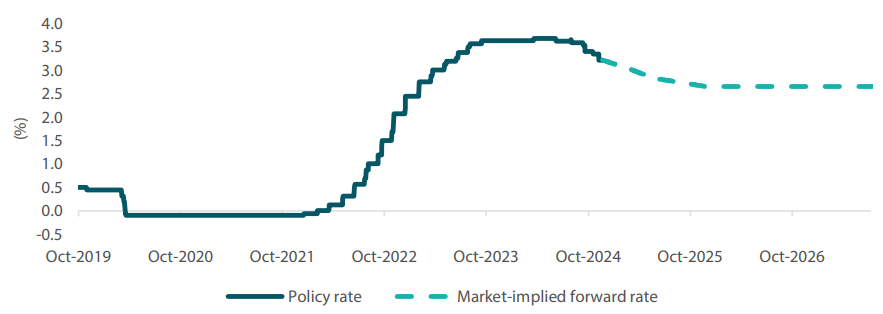

Further policy normalisation on the horizon for Japan

Japan’s monetary policy landscape is poised for a shift, with the Bank of Japan (BOJ) expected to continue with a gradual normalisation of interest rates in the coming quarters. This long-awaited adjustment would mark a significant departure from the country’s prolonged period of ultra-loose monetary policy. The BOJ is expected to deliver another policy rate hike as early as December 2024, with additional hikes expected over subsequent quarters in 2025. While specific figures remain uncertain, the move signals a notable policy pivot aimed at aligning with global monetary trends. Wage growth in Japan has been robust by historical standards, contributing to a gradual recovery in consumer spending. This shift reduces the likelihood of a return to deflation or significant disinflation, supporting the case for normalisation. Normalising policy would likely benefit the Japanese yen, which has been under pressure due to significant differentials between the BOJ’s interest rates and those of other G10 central banks. As interest rate differentials narrow, there is potential for the yen to recover from its currently depressed levels, both nominally and in real terms (Chart 3).

Chart 3: Average G-4 monetary policy rate

Source: Nikko AM, Bloomberg as of 20 November 2024

That said, political dynamics following the snap election called in October 2024—a decision which backfired for the ruling Liberal Democratic Party—have added a layer of uncertainty to the BOJ’s trajectory. The loss of a clear majority by the ruling coalition may lead to greater opposition from parties less supportive of rate hikes. Additionally, discussions of increased fiscal spending could influence the economic outlook and the pace of monetary adjustments.

Credit markets and regional insights

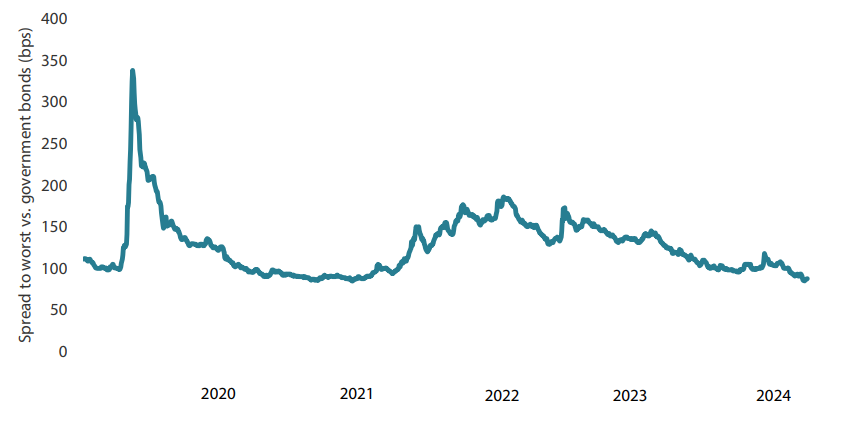

The credit market is currently characterised by tight valuations, with spreads near the lower end of historical ranges. Despite this, we remain cautiously optimistic due to three key factors: fundamentals, technicals and valuations.

From a fundamentals perspective, corporate earnings remain generally strong, with most sectors demonstrating resilience. However, sectors like consumer products and retail are facing headwinds due to a slowing labour market and softer top-line growth. We are more cautious in these areas while remaining constructive on sectors like utilities and real estate, which stand to benefit from lower interest rates. We also remain constructive on banks, which might benefit from a more favourable regulatory environment under the Trump administration.

From a technical perspective, robust inflows into investment-grade corporate bonds continue to support the market. Elevated yields are attracting investors seeking compelling all-in returns, even as spreads remain tight. This dynamic provides a supportive technical backdrop, as long as inflows persist.

And in terms of valuations, while credit spreads appear stretched, all-in yields remain historically attractive, mitigating concerns over tight spreads. Without a clear catalyst for widening spreads, we view the current environment as offering opportunities for selective investment, particularly in high quality credit.

Chart 4: Credit spreads remain tight (ICE BofA Global Corporate Index)

Source: Nikko AM, Bloomberg as at 20 November 2024

Sustainable fixed income: divergence and potential disagreement

The election of Trump means ESG (Environmental, Social, and Governance) as a movement appears effectively dead in the US. From here on, sustainable bond issuance will likely be confined to regional and local government initiatives, particularly in US states with pro-environment policies. US-domiciled corporations are unlikely to pursue ESG-linked debt issuance in this environment.

Despite these challenges, sustainability-linked issuance in dollar terms remains relatively robust, bolstered by reclassifications in key programmes like social housing. This shift has enhanced market liquidity and diversification opportunities. However, it has not significantly changed the broader outlook for US green bonds, which are expected to remain a smaller segment of the global market. In contrast, Europe continues to drive sustainability initiatives, supported by stringent disclosure requirements and a regulatory framework that incentivises sustainable debt issuance. European companies operating globally are subject to these rules, creating a potential point of conflict with US policies.

The divergence between the European Union (EU)’s disclosure standards and the more limited climate-related requirements from the US Securities and Exchanges Commission (SEC) could lead to significant trade and regulatory conflicts. US companies, which are required to comply with EU Corporate Sustainability Reporting Directive standards for European operations but not domestically, will likely face increased costs and the potential for fines from the EU. This tension may escalate, particularly under the incoming US administration, which has shown a willingness to use tariffs as leverage in international negotiations.

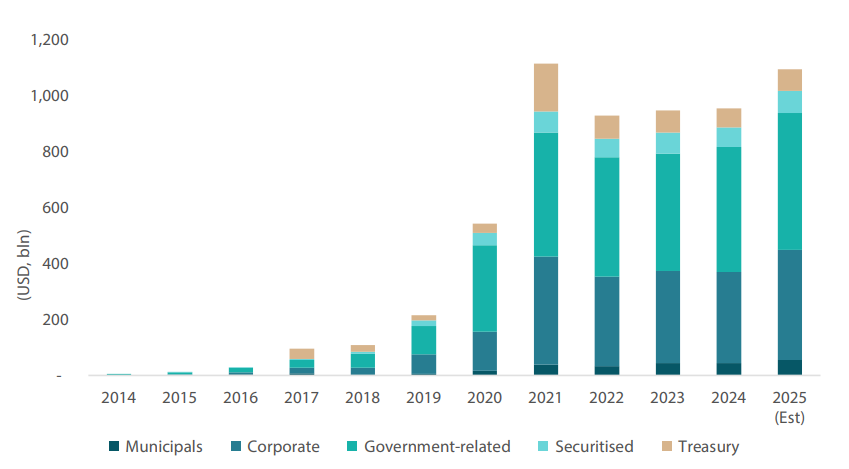

Despite these hurdles, the global green and sustainable bond market continues to expand. Global issuance, including social and sustainability-linked bonds, is on track to approach USD1.0 trillion in 2024 (Chart 5). European issuers dominate, as euro-denominated bonds account for the majority of new issuance. US-based entities are likely to remain underrepresented in this market unless there is a significant policy shift at the federal level, a change that appears unlikely in the near term.

Chart 5: International Capital Market Association-labelled issuance by asset class

Source: Nikko AM, Bloomberg as at 21 November 2024

Conclusion

As Trump begins his new presidential term, there are indications that his approach to governance is evolving. A more pragmatic approach could provide greater clarity and stability for markets in the years ahead. While bond markets have reacted cautiously, pricing in concerns about inflationary risks, we believe these fears are overblown. The prospect of a significant resurgence in inflation appears limited given the disinflationary trends already in place. Instead, this initial market reaction could present a buying opportunity for fixed income investors, particularly as clarity around fiscal and monetary policy develops.

We hope the evolving tone of the new Trump 2.0 administration may signal a period of more stable policymaking, with a focus on legacy-building and long-term impact. For investors, this environment should present opportunities across asset classes, with fixed income in particular poised to benefit as markets adjust to more realistic inflation expectations.