The US tariff-induced turmoil could slow the pace of the Bank of Japan’s rate hikes, but the cycle of wages and prices, which has made the central bank confident about monetary tightening, is expected to remain intact over the longer term.

Impact of US tariffs may slow BOJ rate hikes, but underlying scenario of resilient consumption remains unchanged for now

Early in April, on what was dubbed “Liberation Day”, the US imposed a so-called reciprocal tariff of 24% on goods it imports from Japan. The tariff rate was higher than many expected, and in an initial reaction the Nikkei Stock Average fell sharply along with its regional peers on fears of an intensifying trade war having a detrimental effect on the global economy. During the plunge the Nikkei plumbed its lowest level since October 2023. However, as of this writing the index has since pulled back from the lows, and the market appears to have priced in the worst during its plunge.

The immediate focus is on how Japanese Prime Minister Shigeru Ishiba can negotiate with Washington in a bid to lower the tariffs imposed on Japan. Ishiba may have a few cards to play, including potential purchases of Alaskan natural gas and imports of US-made defence equipment. Another focal point is how individual firms try to cope with higher US tariffs, with many expected to consider enhancing their manufacturing capacities in the US.

Another focal point is the impact the US tariff-induced turmoil could have on Bank of Japan (BOJ) monetary policy. In January, the BOJ raised the short-term policy rate by 25 basis points to 0.5%, its highest since 2008. The rate hike was the BOJ’s second tightening move after it lifted the policy rate from 0% to 0.25% in March 2024. Before the US tariffs were imposed, the central bank was seen to be on a gradual rate hike trajectory, but the pace of its tightening could slow in the wake of the recent market turmoil.

However, that is not to suggest that the cycle of wages and prices, which made the BOJ confident about hiking rates, will fade. Our view is that the original scenario, in which resilient domestic consumption supports a recovery by equities in the second half of 2025 thanks to a continued rise in wages and slowing inflation, remains unchanged.

BOJ Governor Kazuo Ueda said at a parliamentary session in late March that the central bank could hike rates if persistent increases in food costs lead to broad-based inflation. Japan is said to be going through a second wave of a rise in food costs, exemplified by a surge in the price of rice, which is a staple in the Japanese diet. Ueda touched upon a complex subject from a central bank’s perspective, as the BOJ does not have the means to directly impact food prices. That the BOJ governor mentioned food prices is significant, not because the central bank is simply expected to counter higher food costs with monetary policy, but as he seems to be focused on the possibility of consumers not being deterred from buying other items even if faced with higher food costs.

The price of rice may be monitored closely in the coming months, as it could serve as a litmus test to see if consumers continue purchasing discretionary items even if the cost of the staple continues to increase. If consumers carry on buying discretionary items even when the price of rice rises, the BOJ can infer that such behaviour is being supported by wage increases and therefore conclude that inflation is genuine.

Japanese equities lacklustre in March amid concerns over trade, US economy

The Japanese equity market was lacklustre in March with the TOPIX (w/dividends) up 0.22% on-month and the Nikkei 225 (w/dividends) falling 3.34%. Excessive concerns regarding the US economy receded following the release of US economic indicator data, and anxieties surrounding US trade policy, including “reciprocal tariffs” to be implemented in April, also eased somewhat following reports that US President Trump could possibly carve out tariff exemptions for many countries, both positive factors supporting Japanese stocks. However, overall the market was weighed down by investors’ growing risk-off sentiment against a backdrop of negatives such as a TV interview where Trump refused to explicitly deny the possibility that the US economy could enter a recession due to the impact of tariffs and other economic policies, in addition to the announcement that the US plans to levy additional tariffs on imported autos.

Of the 33 Tokyo Stock Exchange sectors, 15 sectors rose with Mining, Insurance, and Real Estate among the most significant gainers. In contrast, 18 sectors declined, including Marine Transportation, Other Products, and Services.

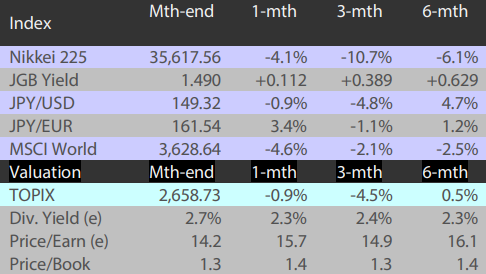

Exhibit 1: Major indices

Source: Bloomberg, 31 March 2025

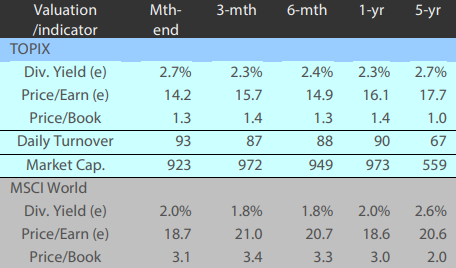

Exhibit 2: Valuation and indicators

Source: Bloomberg, 31 March 2025