Summary

- US Treasuries (USTs) began 2025 on a weak note, with yields rising amid substantial supply pressure. UST yields pulled back later in January after the December 2024 US headline consumer price index (CPI) came in line with expectations; meanwhile, the core CPI was slightly softer than anticipated. Toward the end of the month, the US Federal Reserve (Fed) held interest rates steady, following three consecutive rate cuts. At the end of January, the benchmark 2-year and 10-year UST yields had settled at 4.20% and 4.54%, respectively, 4.4 basis points (bps) and 3.1 bps lower compared to end-December.

- Within Asia, Indonesia surprised with a rate cut to prioritise economic growth. Singapore also eased its monetary policy stance for the first time since 2020. Headline inflation prints for December were mixed across the region. Inflationary pressures increased in Thailand, Indonesia and the Philippines while subsiding in China, India and Malaysia.

- With lower market volatility, we believe that Asia's local government bonds are well-positioned for decent performance in 2025. We see Asian local government bonds being supported by accommodative central banks amid an environment of benign inflation and moderating growth. Within the region, we expect investor appetite for higher carry bonds such as those of Malaysia, Indonesia and the Philippines to stay firm relative to their regional peers.

- Asian credits generated gains of 0.46% in January despite credit spreads widening 1.6 bps, as UST yields declined. Stronger USTs led Asian investment grade (IG) credits to outperform Asian high-yield (HY) credits, with IG credits returning +0.52%, as spreads narrowed by 1.2 bps. Asian HY credits returned +0.08% despite spreads widening by 13 bps.

- Against a benign macro backdrop, we expect Asian corporate and bank credit fundamentals to stay resilient, aside from a few sectors and specific credits which may be impacted by tariff threats or US policy changes. Overall revenue growth may see some moderation, but it should still remain at healthy levels, with profit margins holding steady due to lower input costs. With the removal of the weakest credits from the Asia HY space, we expect the Asia credit default rate to continue declining. We also expect a smaller percentage of fallen angel credits in the Asia IG space.

Asian rates and FX

Market review

The Fed hits the pause button on recent interest rate cuts

USTs began 2025 on a weak note, with yields rising amid substantial supply pressure. A robust US employment report prompted markets to significantly recalibrate expectations for further Fed rate cuts, pushing yields even higher. UST yields pulled back later in January after the December 2024 US headline consumer price index (CPI) came in line with expectations; meanwhile, the core CPI was slightly softer than anticipated. Yields fell further after US President Donald Trump provided some clarity on his policies in his inauguration speech, particularly as he made no reference to imminent tariffs. Towards the end of the month, the Fed held interest rates steady following three consecutive rate cuts. Notably, the Fed's post-meeting statement adopted a more optimistic tone about the labour market. The Fed also excluded a key reference from its December 2024 statement that acknowledged inflation was progressing toward its target. At the end of January, the benchmark 2-year and 10-year UST yields settled at 4.20% and 4.54%, respectively, 4.4 bps and 3.1 bps lower compared to end-December.

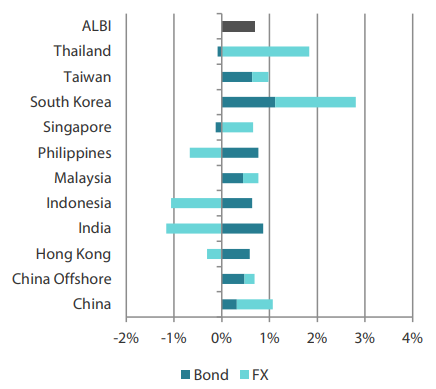

Chart 1: Markit iBoxx Asian Local Bond Index (ALBI)

For the month ending 31 January 2025

Exhibit 2: Valuation and indicators

Source: Markit iBoxx Asian Local Currency Bond Indices, Bloomberg, 31 January 2025.

BI lowers policy rate; MAS eases its foreign exchange policy

Bank Indonesia (BI) lowered its benchmark seven-day reverse repo rate by 25 bps to 5.75% in January, prioritising growth support and defying expectations that it would maintain policy settings to stabilise the Indonesian rupiah. The central bank now forecasts growth of between 4.7% and 5.5% in 2025 (from 4.8-5.6%), citing challenges such as weak exports, sluggish household consumption and limited private investment. For 2024, growth is expected to fall slightly below the midpoint of the 4.7-5.5% range, primarily due to muted domestic demand, according to BI Governor Perry Warjiyo.

In Singapore, the Monetary Authority of Singapore (MAS) eased its foreign exchange policy for the first time in almost five years. It announced a slight reduction in the slope of the Singapore dollar nominal effective exchange rate (SGDNEER) policy band while leaving the width of the band and the level at which it is centred unchanged. The MAS highlighted rising global economic uncertainty, which it described as mainly driven by expectations of increasing trade policy frictions and projected a moderation in economic growth for 2025. However, it maintained its 2025 gross domestic product (GDP) growth forecast at 1-3%. While the headline inflation forecast for 2025 remained unchanged at 1.5-2.5%, MAS revised its core inflation projection to a lower range of 1-2%, down from the previous estimate of 1.5-2.5%.

In contrast, central banks in South Korea and Malaysia held their respective policy rates steady. Bank Negara Malaysia highlighted narrowing interest rate differentials with advanced economies as a positive factor for the Malaysian ringgit. It noted that while global policy uncertainties may spur market volatility, the ringgit remains supported by strong economic prospects, domestic structural reforms and initiatives to boost capital flows. Meanwhile, the statement from Bank of Korea (BOK) accompanying its decision to stay pat on interest rates noted that weaker exports and declining consumer sentiment would likely slow 2025 economic growth below its earlier forecast. BOK Governor Rhee Chang-yong noted that the decision to leave rates unchanged was partly aimed at supporting the South Korean won. He added that six of the seven board members agreed that the central bank should be open to further rate cuts in the next three months.

December headline CPI prints mixed across the region

The headline CPI numbers for December 2024 were mixed across the region. Inflationary pressures rose in Thailand, Indonesia, and the Philippines, remained stable in Singapore, and eased in China, India, and Malaysia.

Thailand's headline inflation rate returned to the central bank's target range for the first time since May 2024, rising to 1.23% year-on-year (YoY) in December from 0.95% in November, lifted by higher raw food and energy prices. In the Philippines, the headline CPI rose to 2.9% YoY, up from 2.5% in November, due partly to faster increases in housing, water, light and fuel costs. Singapore's overall inflation held steady at 1.6% YoY but it was slightly above expectations of 1.5%, as lower core and accommodation inflation offset a smaller decline in private transport costs. Elsewhere, Malaysia saw its headline CPI ease to 1.7% YoY in December, slightly down from 1.8% in November, mainly due to slower price growth in health, communication, recreation/culture and miscellaneous categories.

Singapore, South Korea and Malaysia register slower growth in the fourth quarter

According to advance estimates, Singapore's economy grew by 4.3% YoY in the fourth quarter of 2024, slowing from the previous quarter's 5.4%. For the full year, Singapore's GDP expanded by 4.0% in 2024, significantly outpacing the 1.1% growth recorded in 2023. Similarly, Malaysia's economy lost momentum in the fourth quarter, with GDP rising 4.8% YoY—below market expectations of 5.2% and down from 5.3% in the third quarter. For 2024, the economy grew by 5.1%, within the government's projected range and exceeding the 3.6% growth achieved in 2023. In South Korea, the economy expanded by only 1.2% YoY in the final quarter of 2024, down from the previous quarter's 1.5% and falling short of the expected 1.4% increase, largely due to sluggish consumption and a slowdown in the construction sector. For the full year, GDP growth reached 2.0%, an improvement from the 1.4% recorded in 2023.

In China, fourth-quarter GDP growth exceeded market expectations and accelerated to 5.4% YoY, up from the previous quarter's 4.6%. For the full year, real GDP growth reached 5% in 2024, meeting the government's official target but slowing from 5.2% in 2023. Policymakers attributed the annual growth largely to gains in investment and exports, which helped offset weaker consumption. Meanwhile, the Philippine economy maintained a steady growth rate of 5.2% YoY in the fourth quarter, matching the previous quarter. However, full-year growth stood at 5.6%, falling short of the government's target.

Market outlook

Remain constructive on higher carry bonds

With lower market volatility, we believe that Asia's local government bonds are well-positioned for a decent performance in 2025. We see Asian local government bonds being supported by accommodative central banks amid an environment of benign inflation and moderating growth. The ongoing global easing cycle is expected to drive down global yields and also support Asian bond markets. Furthermore, we expect global growth to moderate in the medium term, driven in part by potential tariff threats from the US. This scenario is likely to support bond markets overall. Within the region, we expect appetite for higher carry bonds such as those of Malaysia, India, Indonesia and the Philippines to stay firm relative to regional peers.

Amid the uncertainties surrounding the Trump administration, we remain broadly cautious on Asian currencies in the near term. However, we see the region's strong economic fundamentals cushioning the impact, with the Malaysian ringgit as our preferred currency.

Asian credits

Market review

Asian IG credits see a strong start to the year

As UST yields declined, Asian credits posted gains of 0.46% in the first month of 2025 despite credit spreads widening 1.6 bps. Stronger USTs prompted Asian IG credits to outperform Asian HY credits, with IG credits returning +0.52%, as spreads narrowed by 1.2 bps. Asian HY credits returned +0.08% despite spreads widening by 13 bps.

Asian credit spreads remained largely range-bound in January, despite volatility in UST bonds and busy primary market activity. However, performance across IG and HY credit were mixed. While IG credit held steady on strong technicals, HY credits experienced notable weakness in the second half of the month, largely driven by negative sentiment in the Hong Kong HY property sector. Concerns over the situation of a large Hong Kong developer and the possibility of a restructuring exercise prompted a significant sell-off in Hong Kong property credits and a widening of Hong Kong bank credits. China's property credits weakened in the first half of the month on increasing concerns around a large Chinese developer's liquidity and reports that its CEO had been arrested. However, they subsequently recovered along with signs that the government may step in to provide support.

By the end of January, credit spreads of India, Indonesia, Macau, Singapore, South Korea and Taiwan had tightened, while those of China, Hong Kong, Malaysia, Thailand and the Philippines had widened. Notably, gains in the India-based Adani group led the performance of Indian credits.

Primary market activity surges in January

After a very quiet December, primary market issuance surged at the start of 2025, reaching USD 26.8 billion. The IG space saw a remarkable 32 new issues, totalling USD 24.5 billion, with a significant portion coming from sovereign and quasi-sovereign issuers. Notable issues included the massive USD 4.15 billion three-tranche issue from Airport Authority Hong Kong, the USD 3 billion four-tranche issue from Export Import Bank of Korea, the USD 3.0 billion three-tranche issue from Korea Development Bank, the USD 2.5 billion three-tranche issue from Standard Chartered PLC, the USD 2.25 billion two-tranche sovereign issue from the Philippines and the USD 2.0 billion two-tranche sovereign issue from Indonesia. Meanwhile, the HY space saw six new issues totalling USD 2.3 billion.

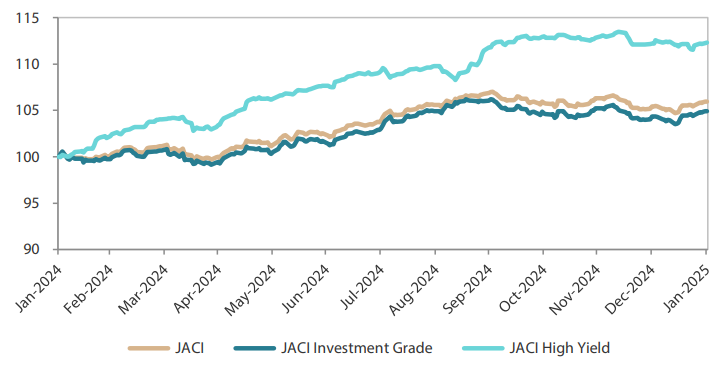

Chart 2: JP Morgan Asia Credit Index (JACI)

Index rebased to 100 at 31 January 2024

Note: Returns in USD. Past performance is not necessarily indicative of future performance.

Source: Bloomberg, 31 January 2025.

Market outlook

Asia credit yields remain attractive; spreads likely to be bound in range, returns to be driven by carry

We expect Asia credit fundamentals to stay resilient in 2025. China is expected to maintain efforts to rebalance its economy, adopting more accommodative policies to mitigate the effects of a challenging external landscape due to US tariff risks, and to stabilise overall growth. Asia ex-China macroeconomic fundamentals may moderate slightly from the robust levels seen in 2024 as export growth comes under pressure, but they are expected to remain resilient overall. We believe Asian central banks have ample room to ease monetary policy to bolster domestic demand.

Against a benign macroeconomic backdrop, we expect Asian corporate and bank credit fundamentals to also stay resilient, aside from a few sectors and specific credits which may be affected by tariff threats or US policy shifts. Overall revenue growth could moderate but is expected to stay at healthy levels, with profit margins holding steady due to lower input costs. We expect most Asian corporates and banks to have started 2025 with strong balance sheets and adequate rating buffers. As the weakest credits in the Asia HY space have been removed, we expect default rates to decrease in 2025. We also expect a smaller percentage of fallen angel credits in the Asian IG space.

We anticipate an increase in gross supply in the Asia credit space in 2025 compared to the past two years, as the decline in US yields reduces the funding cost gap between offshore and onshore debt. Many regular issuers may also wish to refinance in the USD-denominated market to maintain a longer-term presence. However, net supply will likely be subdued given still elevated redemptions. At the same time, we expect demand from regional investors to stay firm given the still high all-in yield.

While credit spreads are historically tight, the combination of supportive macroeconomic and corporate credit fundamentals, along with robust technicals, are expected to keep spreads mostly bound in range in 2025. We remain cautiously optimistic and prefer the cross-over BBB- and BB-rated credit space trading in the low-to-mid 200 bps spread. We anticipate carry to be the main driver of Asia credit returns in 2025.