The biodiversity financing gap

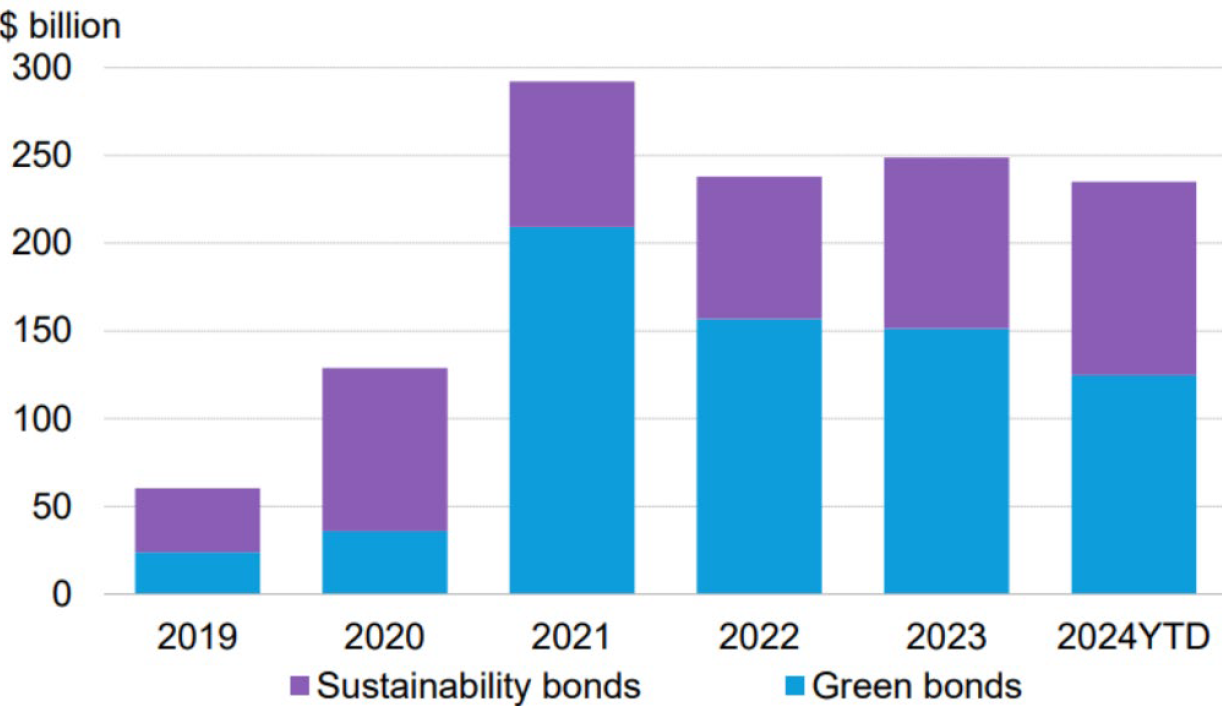

While climate finance has grown substantially in recent years, biodiversity-focused investment still lags behind. According to BloombergNEF (BNEF), biodiversity constituted just 1% of total green bond use of proceeds in 20241. In another report prepared ahead of the UN Biodiversity Conference (COP16)2 held at the end of October 2024, BNEF noted that while the annual issuance of green bonds with biodiversity use-of-proceeds has hovered between USD 200 billion and USD 300 billion since 2021, only 3.7% of the funds raised through these bonds in 2021–2022 were actually allocated to biodiversity-specific projects.

Chart 1 – Green and sustainability bond issuance with biodiversity use of proceeds

Source: BloombergNEF, Bloomberg Terminal. Note: Use of proceeds (UOP) data represents a maximum that could be allocated to biodiversity activities. Allocation data excludes portfolio level allocation disclosures. Data through August 2024.

Estimates of the biodiversity financing gap further illustrate the challenge: the Paulson Institute has estimated the shortfall at USD 711 billion per year3, while BNEF reported in 2024 that the gap had widened to USD 942 billion, driven in part by inflation and stagnant investment levels.

This is not due to a lack of awareness or demand, but rather, a lack of suitable, investable opportunities. Most nature-positive projects—such as ecosystem restoration, protected area management, or floodplain rehabilitation—are long-term, systemic, and not always easily monetised.

Across public equity and corporate bond markets, direct exposure to biodiversity projects remains limited. Green bonds issued by companies have made impressive strides in climate mitigation and energy transition financing. However, biodiversity is often not financially material for most sectors, or only relevant to a subset of issuers such as water utilities, forestry, or agribusiness. For many corporates, it remains difficult to identify biodiversity-related projects that are both financially significant and well-suited to the green bond format.

This is where we believe sovereign green bonds can play a critical role.

Why sovereigns are uniquely positioned

Sovereign issuers are responsible for managing large areas of land and water, along with national biodiversity assets that are central to public policy. They have the mandate, scale, and long-term planning horizons required to fund nature-positive investments that deliver public goods—often with benefits that unfold over decades.

National governments are also more likely to link such investments to broader policy objectives, such as climate adaptation, disaster risk reduction, rural development, or environmental protection. This creates a natural alignment between green bond proceeds and biodiversity outcomes, and positions sovereigns as essential actors in scaling up nature finance. We are already seeing early examples of this approach in action.

Examples of sovereign biodiversity bonds

Italy’s inaugural green bond, issued in 2021, earmarked over 11% of its proceeds to biodiversity and environmental protection. This included soil protection, measures against hydrogeological risk, water infrastructure, and funding for Marine Protected Areas, Nature Parks, and State Nature Reserves. These are systemic projects of national relevance—types of investments that are typically outside the scope of corporate green bonds.

At COP16 in 2024, Colombia issued the world’s first sovereign bond explicitly focused on biodiversity. Structured with support from the IFC and IDB Invest, the bond funds Colombia’s National Biodiversity Strategy, including ecosystem restoration, forest protection, and biodiversity monitoring. This landmark issuance demonstrates how sovereigns can integrate biodiversity into green bond frameworks in a way that reflects national priorities and multilateral commitments.

These examples are still the exception rather than the norm. Most sovereign green bonds to date have focused on energy transition, clean transport, or climate resilience4. However, the increasing availability of well-defined taxonomies, standards, and disclosure frameworks could help shift the landscape.

Building momentum through frameworks and transparency

As interest in nature finance grows, investors are seeking more consistent and transparent ways to allocate capital to biodiversity-related projects. The development of international frameworks such as the Global Biodiversity Framework (adopted at COP15) and the Taskforce on Nature-related Financial Disclosures (TNFD) is expected to play a catalytic role. These initiatives aim to improve how nature-related risks, dependencies, and outcomes are measured and reported—giving both issuers and investors greater clarity and comparability.

Reporting on biodiversity can be challenging and can be embedded in other types of infrastructure or projects, making it difficult to track and report on. For issuers like sovereigns, these frameworks offer tools to structure nature-positive investments within green bond programs and provide more comprehensive visibility into nature-related finance. For investors, they enhance confidence in the integrity and impact of their allocations. Over time, they may help expand the pool of investable nature projects, making it easier for green bonds—sovereign and beyond—to include credible biodiversity use-of-proceeds.

Looking ahead

Sovereign green bonds are not the only path to financing biodiversity, but they are one of the most promising. By enabling governments to fund public-good projects that are difficult to monetize or scale via private markets, they fill a crucial gap in the investment landscape.

Italy and Colombia have shown that it is possible to embed biodiversity in sovereign green bond frameworks with purpose and credibility. As reporting standards evolve and investor demand for nature-positive outcomes grows, sovereign issuers will have an increasingly important role to play in bridging the biodiversity finance gap.

For investors seeking transparent, long-term exposure to nature-related projects, sovereign green bonds represent an important piece of the solution.

If you have any questions on this report, please contact:

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.

1 BENF Sustainable Finance Market Outlook 1H 2025 (p.11)

2 https://assets.bbhub.io/professional/sites/24/Biodiversity-Finance-Factbook_COP16.pdf

4 BNEF Sustainable Finance Market Outlook 1H 2025 (p.12)