Snapshot

October was a negative month for most asset classes, with both bonds and equities dropping for the month. The MSCI World Index fell by a little over 2%, with the S&P 500 dropping 0.99% as earnings results were received with mixed reactions. For example, within the "Magnificent 7", Alphabet and Amazon rose while Microsoft earnings beat expectations, but the market sold off due to the forward guidance being perceived as negative. In addition to earnings news, the market saw volatility rise ahead of the US presidential election, and the market swung up and down as Republican odds of victory ebbed and flowed. However, despite the hiccup in equity market performance, year-to-date returns remain extremely strong with the MSCI World Index up over 15% and the S&P 500 over 20%.

Outside of the equity market, the bond market also experienced some pain in October, with the Bloomberg Global Aggregate Bond Index falling 2.48% as the US 10-year Treasury rose some 50 basis points (bps) to end the month at 4.28%. Despite the 50 bps interest rate cut from the US Federal Reserve (Fed) in September, the market pushed bond yields higher and repriced the terminal cash rate expected in 24 months' time. In addition, as the Republican odds of winning the US elections rose, the market viewed this as negative for the US bond market and pushed both nominal yields and break-even inflation rates higher. With Republicans winning the elections, corporate tax cuts and tariffs are likely to be implemented; such measures are generally viewed as inflationary by the market. Additionally, after weakening for a number of months, the US dollar began to rise, ending a relatively tough month for financial markets.

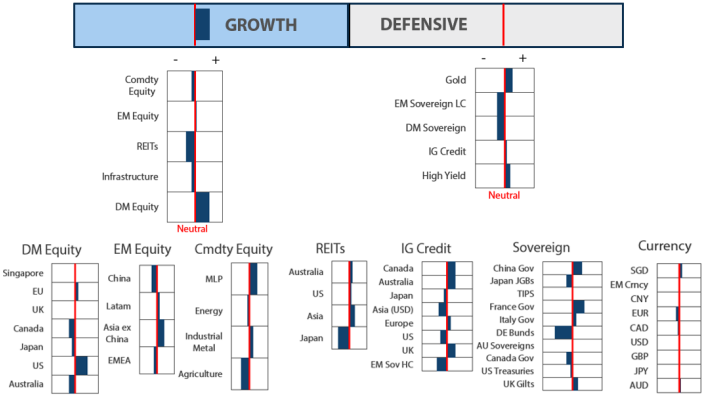

Cross-asset 1

For the month of October, we increased our overweight growth position and maintained a neutral position on defensives. With respect to growth assets, our view of risk assets improved on the start of the Fed's rate cutting cycle, and with a Republican presidency beginning soon. US data continues to show signs of strength, and despite a weather-affected payrolls number, GDP continues to grow above trend. As the Fed continues cutting rates, we expect this favourable economic outlook to be kept intact, sustaining a Goldilocks situation for the near term. Additionally, recent earnings results from US companies have been positive, with a slightly above-average number of companies beating earnings estimates. On the defensive side, we remain neutral despite ongoing rate cuts, as bond curves are quite flat and this makes owning long-dated sovereign bonds relatively tricky.

Within the cross-asset scores of growth, we increased our overweight in developed market (DM) equities and reduced our overweight on emerging market (EM) equities on the back of the US elections results. The red sweep by the Republicans means higher risk of import tariffs and inflation which implies a higher dollar. This reverses our earlier positive view towards EM—an outlook which was accompanied by expectations of a weaker dollar. Meanwhile, we retain our positive view on growth amid resilient economic data and dovish monetary policies globally. We rebalanced our risk exposures by adding to the DM and reducing our overweight positions in EM. We maintained our marginal overweight in Europe while retaining our preference for US on the back of better visibility driven by secular growth themes. We continue to like Japan for its longer term structural story of improving corporate governance and earnings growth momentum but retained the underweight position on the near-term headwinds of yen volatility. However, we would look to add capital on market corrections. We increased our underweight in energy, seeing how pessimism has grown amidst growing oversupply and slowing demand. Instead, we added to the more defensive MLP assets. Within infrastructure, we retained our preference for US utilities to reflect our positive view on increasing energy demand with the secular growth of data centres. Within EM, we continue to like selective countries like India and Indonesia which are expected to benefit from domestically-driven economies and structural long term growth stories. Likewise, we retained our overweight position in Taiwan which is a beneficiary of the current global tech upcycle.

Within defensives, high yield (HY) was increased to a larger overweight while DM and EM sovereigns were downgraded to larger underweights. The shift this month reflects the positive view of the economic environment taking shape following a Republican win, with the incoming Trump administration expected to pursue business-friendly policies. The incoming administration is viewed as friendly towards businesses and if taxes are cut at a time when the Fed is easing rates, corporate conditions are expected to improve. We used this as an opportunity to move into a larger HY position, and additionally, increase our European HY where falling rates are seen benefiting outright yields. For DM sovereigns, we reduced the score to fund the increase in spread products. We reduced our DM sovereign score because the Republican win is seen as inflationary and therefore potentially complicates the Fed's easing program. Despite a tougher bond environment in the US, we still see Europe, Canada and the UK as relatively favourable for bonds. Inflation has dipped below 2% in most of these countries and their low growth rates could result in a number of easing measures. France is our key overweight in the sovereign market, as its wide spread versus Bunds and steep curve makes the country more attractive from a carry perspective.

1 The Multi Asset team's cross-asset views are expressed at three different levels: (1) growth versus defensive, (2) cross asset within growth and defensive assets, and (3) relative asset views within each asset class. These levels describe our research and intuition that asset classes behave similarly or disparately in predictable ways, such that cross-asset scoring makes sense and ultimately leads to more deliberate and robust portfolio construction.

Asset Class Hierarchy (Team View2)

2 The asset classes or sectors mentioned herein are a reflection of the portfolio manager's current view of the investment strategies taken on behalf of the portfolio managed. The research framework is divided into 3 levels of analysis. The scores presented reflect the team's view of each asset relative to others in its asset class. Scores within each asset class will average to neutral, with the exception of Commodity. These comments should not be constituted as an investment research or recommendation advice. Any prediction, projection or forecast on sectors, the economy and/or the market trends is not necessarily indicative of their future state or likely performances.

Research views

Growth Assets

Growth assets are attractive given that economic data remains resilient against falling inflation and as global central banks lower interest rates as they shift away from restrictive monetary policies. The US elections which resulted in a Republican red sweep could lead to increased fiscal spending and higher import tariffs, potentially reigniting inflationary pressures. This could mean a higher-for-longer interest rates outlook and a stronger dollar, which in turn may change our investment perspective. However, expectations towards the Trump administration implementing corporate tax cuts, along with the current rate-cutting cycle, remain powerful drivers of returns. We view any current market corrections as attractive entry points to add on our positions on longer term secular growth story.

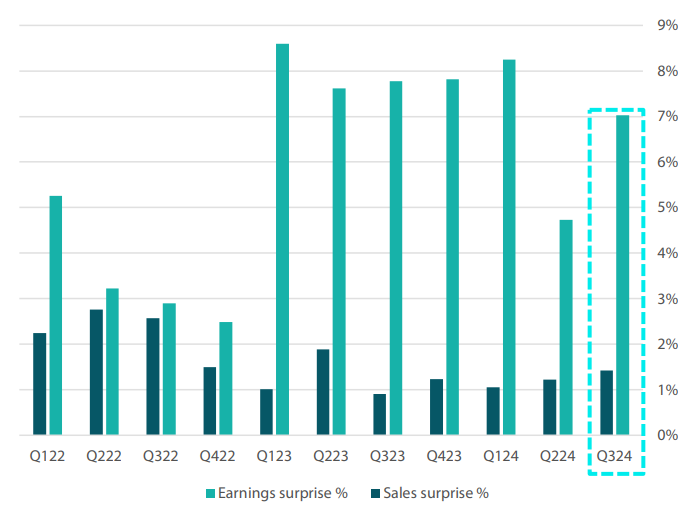

Q3 earnings season scorecard

More than 90% of S&P 500 companies have reported their third-quarter (Q3) earnings and their results have been more resilient than expected, with 75% of these companies reporting earnings beats when compared to the historical average of 74%. Among the companies that reported, 53% also exceeded market sales expectations, which is in line with the historical average. The quantum of the earnings beats, at +7%, is better than Q2 (See Chart 1) and is close to previous peaks in 2023. Likewise, sales beats, at +1.4%, were the highest since Q2 2023.

Chart 1: S&P 500 companies' Q3 earnings and sales beats quantum stronger than the previous quarter

Source: Bloomberg, November 2024

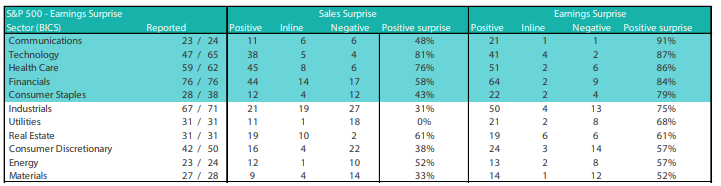

Drilling deeper into sector earnings, communications, technology, healthcare, financials and staples were the standout winners in the reporting season (see Table 1). Communication software companies such as Alphabet and Meta reported top line and bottom line beats amid strong demand for cloud and mobile advertisements. Likewise, semiconductor companies such as Cadence and AMD continued to report strong artificial intelligence (AI)-related demand. On the other hand, deep cyclical sectors such as energy and materials continued to struggle with a softening in commodity prices stemming from weak demand and oversupply.

Table 1: Selective sectors shone during this quarter

Source: Bloomberg, November 2024

In terms of equity performance, financials have been the best performing sector quarter-to-date since reporting started, with technology coming in second. Both sectors rallied strongly on the back of Trump's US elections win, which investors view positively due to expectations of less scrutiny and regulation within these sectors. Financials also rose on the higher-for-longer interest rates rhetoric and as the incoming Trump administration is expected to implement more economic stimulus. Healthcare, on the other hand, was sold down as investors anticipate substantial changes to the US Affordable Care Act (ACA), which could lead to the expiration of subsidies in 2025 and Medicaid funding cuts.

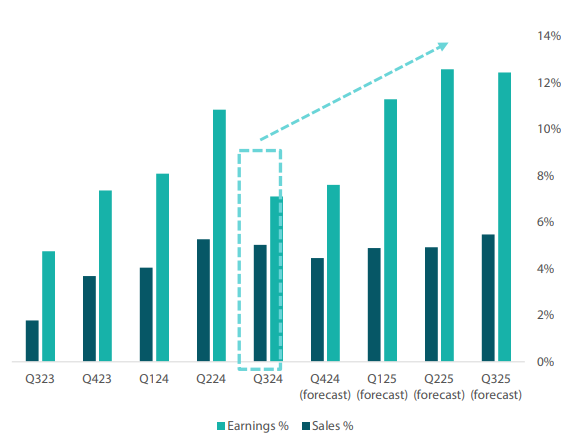

Looking through the earnings growth expectations of the market, it is worth noting that Q3 represents a trough for US earnings growth in 2024. We expect to see earnings growth to accelerate henceforth (Chart 2), especially with the incoming Trump administration expected to implement tax and interest rate cuts in the coming quarters.

Chart 2: S&P 500 companies' earnings and sales growth expected to accelerate after reaching trough in Q3

Source: Bloomberg, November 2024

Conviction views on growth assets

-

Maintain exposure to US secular growth:

We continue to like US tech-related stocks despite market concerns regarding the returns expected on investments made on AI and data centres. Corporate earnings have been holding out well, and the

secular long- term growth story for the sector remains intact. Within the US, we are also starting to see the rally widening beyond the "Magnificent 7", which is positive for the overall market.

As inflation comes under control amidst a more dovish monetary policy, risk assets should do well in US. Likewise, the red sweep by the Republicans is positive for equity markets as we expect to

see continued strong fiscal spending and protectionism from the US to support its economy.

Reduce exposure to EMs: We decreased our overweight position in EMs on the back of the Republicans' red sweep. We maintain our view that interest rate cuts will continue into 2025; however, the pace will likely slow, resulting in a stronger-than-expected dollar. A strong dollar historically would present headwinds for EM performance as central banks in the region will have less leeway to cut rates to stimulate their domestic economies. Within EMs, we still like selective markets in India and Indonesia which benefit from domestically-driven economies and structural long term growth stories. Likewise, we like Taiwan for its exposure to the global technology upcycle. - Maintain Japan equities: We maintained an underweight in Japan equities due to increasing volatility on the yen. We still like Japan's structural reform story where we expect companies to increase their capital and dividend returns to shareholders. However, the volatility of the yen and a hawkish Bank of Japan juxtaposed against dovish central banks globally also presents headwinds to sentiments. We will turn more positive on the country once we see its currency stabilising at a higher level.

- Remain underweight on commodity-linked equities: Given the slowing economic data and energy oversupply, we retained our underweight exposure in the asset class. We rebalanced the weights from materials and energy equities given weak sentiments and added into MLPs on strong defensive yields and good structural story. We continue to believe that the asset class will continue to provide good diversification against inflation in the longer term. The sector's fundamentals remain compelling due to both cyclical and secular fundamentals.

Defensive assets

Over the past 12 months, the team has been relatively negative on sovereign bonds, and despite the rate-cutting cycle getting underway, we maintain this view. The highly anticipated US economic slowdown never occurred, and with the resumption of a Republican White House in 2025, we expect that this above-trend economic outlook will continue into the near term. Accordingly, we have increased our weight to spread products, and looked to neutralise our duration relative to the Strategic Asset Allocation. This month's Balancing Act looks at some key bond prices during 2017 and 2018 when Trump's first round of tax cuts and tariffs took place.

Trump returns

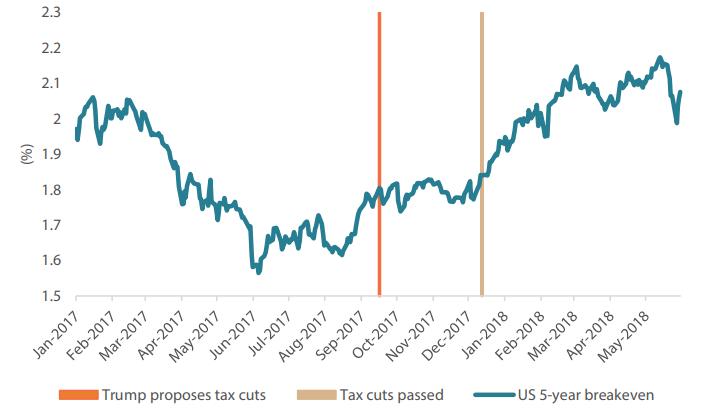

With the Republicans winning the House and thus gaining control of all branches of government, corporate tax cuts are very likely to be proposed. When tax cuts are combined with Trump's affinity for tariffs, this will likely create a more inflationary outlook than previously expected. The market viewed this as a negative for bonds, which sold off in the run up to the elections as the odds of Trump winning the presidency rose. Interestingly in 2017, when Trump proposed and then enacted corporate tax cuts, US 5-year inflation breakeven pricing rose higher (Chart 3). This is similar to what has happened since Republicans won the presidency this time, with break-evens rising 50 bps since September.

Chart 3: US 5-year breakeven inflation pricing (2017-2018 period)

Source: Bloomberg November 2024

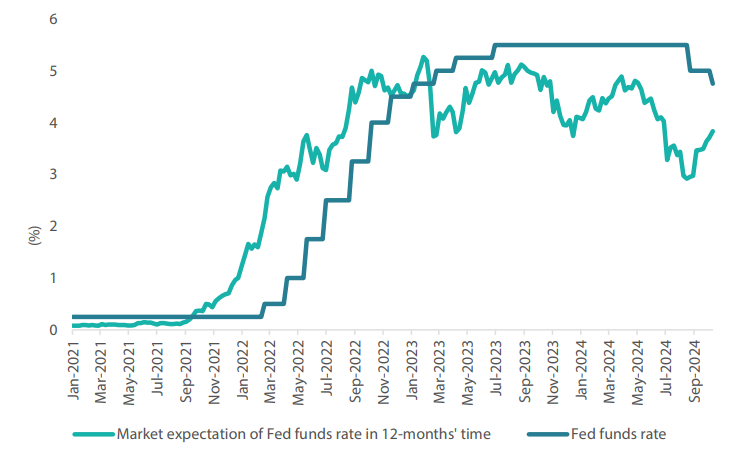

This shifting outlook should make the Fed's job at cooling inflation slightly more problematic, as the combination of tax cuts and tariffs reverses the effects of slowing inflation. In a recent press conference, Fed Chair Jerome Powell stated that in "the near term, the election will have no effects on our policy decisions" and that since they "don't know what the timing and substance of any policy changes will be", the Fed does not guess or assume how the trajectory can change. However, this is not how the market is reading the situation. The market quickly began repricing Fed funds rate expectations as Trump's odds of winning the election rose and has continued to do so after Trump's win. The Fed may not be ready to adjust its view, but the market is suggesting that this is now a more inflationary environment resulting in higher-for-longer interest rate conditions.

Chart 4: US Fed funds rate pricing and Fed funds rate

Source: Bloomberg, November 2024

From a portfolio perspective, this reverses the recent positivity of the past two months and creates a more questionable interest rate environment. We still expect the Fed to cut rates; however, we see the terminal rate being kept in the 3.50% range for some time. Given that US 10-year bond yields typically trade 100 to 200 points over cash, this means we do not see strong value in the sovereign market until 10-year bond yields rise above 4.50%. We continue to prefer bonds from Europe, where economic growth is slow, inflation is below 2% and Trump's tariffs policies could further hurt trade. This scenario could lead to an increase in expectations of more rate cuts from the European Central Bank.

Conviction views on defensive assets

- Short-dated IG credit: Credit spreads remain at fair levels, but many markets still exhibit inverse yield curves, making longer-dated credit less appealing. As curves begin to steepen, we will look to shift this position. However, the current curve inversion still makes short-dated positions appealing.

- Gold remains an attractive hedge: Gold has been resilient in the face of rising real yields and a strong dollar, while proving to be an effective hedge against geopolitical risks and persistent inflation pressures. Falling real yields should benefit the asset class and we use this allocation to supplement our long bond positioning.

- Adding duration: As central banks begin to ease rates, this should be beneficial to bond markets globally. Picking the timing for cuts can be difficult; however, as restrictive policy comes to an end, this should be positive for bonds. We still expect Europe to ease aggressively, with countries such as France and Italy being our preferred allocations for interest rate exposure.

Process

In-house research to understand the key drivers of return:

| Valuation | Momentum | Macro |

| Quant models to assesss relative value | Quant models to measure asset momentum over the medium term | Analyse macro cycles with tested correlation to asset |

| Example for equity use 5Y CAPE, P/B & ROE | Used to inform valuation model | Monetary policy, fiscal policy, consumer, earnings & liquidity cycles |

| Example | ||

| + | N | N |

| Final Score + | ||