Why the market is unfazed by Japan’s upcoming leadership change

On 14 August, Japanese Prime Minister Fumio Kishida announced that he will not run in the ruling Liberal Democratic Party (LDP)’s leadership election scheduled late in September. What this means is that Kishida, whose popularity had plummeted due to a number of scandals that plagued the LDP during his tenure, will be stepping down. Consequently, his successor as leader of the LDP is poised to become Japan’s next prime minister by extension.

The Japanese market took Kishida’s announcement in stride and has not reacted much to political developments since, despite almost a dozen candidates vying for the LDP leadership role. The market’s response has been muted because it expects Kishida’s successor to dissolve the lower house and call a snap election soon after taking office. Kishida’s successor will have unique policy agendas, some with potential implications for the economy and markets. The market, however, may take a wait-and-see approach, focusing fully on the new leader’s policies only after the snap election is over.

The immediate focus will be how much support the ruling party can secure at the snap election. The stronger the support, the more influence the next prime minister will wield in enacting policy. Such influence matters as the next leader could retain some of Kishida’s policies that were considered positive by investors, such as growth strategies for certain industries (including artificial intelligence, semiconductors and space) and initiatives aimed at improving labour market efficiency. While Kishida had some commendable policies, his dwindling popularity hindered his ability to effectively implement them. In this context, Japanese equities could react positively to a landslide victory by the LDP in the snap election, although such a win appears unlikely at this stage. The market is expected to pay more attention to policies aimed at continually improving Japan’s economic structure, rather than those designed to enhance the economic cycle, which many believe is already on a path to recovery.

Each candidate for the next prime minister holds different views regarding monetary policy. For instance, digital minister Taro Kono recently called for the Bank of Japan (BOJ) to hike interest rates. Conversely, economic security minister Sanae Takaichi is seen to favour monetary easing. However, it is worth noting that policymakers generally avoid delving too deeply into monetary policy. Those who do—such as the late Prime Minister Shinzo Abe—are more the exception than the rule. The BOJ is therefore expected to maintain its monetary tightening trajectory. Even if ruling party policymakers were to voice their opinions on monetary policy under the new administration, the BOJ is likely to deflect such pressure through measures such as issuing formal statements.

Foreign bid for iconic store operator shows that Japan Inc. looks like a bargain

The market experienced a stir in August when an operator of a prominent chain of convenience stores—ubiquitous throughout Japan and considered a cultural icon—received a buyout bid from a Canadian counterpart. Although it is uncertain whether the buyout will actually proceed at the time of this writing, the Canadian firm’s proposal served as a reminder to domestic market participants and investors that Japanese companies look like bargains in the eyes of their foreign peers.

The primary reason Japan Inc. looks affordable is the weakness of the yen. The Japanese currency has managed to recover somewhat from its multi-decade lows beyond 160 to the dollar reached in July and currently trades in the mid-140 range versus the greenback. However, from a historical perspective the yen is still weak. Prolonged yen weakness may expose Japanese companies to a new form of foreign influence. In the past, foreign influence came primarily from activists proposing changes to existing management. However, the buyout proposal for the Japanese convenience store operator showed that foreign entities, perhaps motivated in part by a weak yen, can buy Japanese companies outright and attempt to remould the management after the purchase.

The weak yen could also heighten interest in ongoing corporate governance reforms. From a foreign buyer’s view, acquiring a company where reform is already underway may be more appealing than buying a firm at which reforms still need to be initiated. From a domestic firm’s perspective, implementing reforms and increasing its own share price could be a strategy to avoid a buyout. What should be noted, however, is that any share price improvements resulting from reforms could be easily overshadowed should the yen weaken further.

This is not to suggest that if the yen depreciates, Japanese companies will be purchased in large numbers. Many potential buyers may hesitate to acquire Japanese companies based solely on favourable exchange rates, given the significant post-M&A management challenges each acquisition may bring due to factors such as language barriers and cultural differences. Considering these potential obstacles, buyers may be more inclined to target firms with established business models that could be exported outside of Japan.

August market summary: Japanese equities slip amid the yen’s appreciation

The Japanese equity market ended August lower with the TOPIX (w/dividends) down 2.90% on-month and the Nikkei 225 (w/dividends) falling 1.09%. At the start of the month, stocks tumbled as expectations diminished regarding Japanese exporters’ earnings amid the yen’s appreciation against the US dollar, in addition to heightening concerns of an economic slowdown in the US due to weaker-than-expected economic indicators for the US manufacturing industry and labour market. However, later on such excessive concerns about the direction of the US economy eased following the release of US ISM non-manufacturing PMI figures which exceeded market expectations, while in Japan preliminary data showed that gross domestic product grew more than expected in real terms in the April-to-June quarter. These positives, combined with expectations that the US Federal Reserve could cut rates at an early stage based on Fed Chair Jerome Powell’s remarks, lifted Japanese equities later in the month.

Of the 33 Tokyo Stock Exchange sectors, 10 sectors rose, with Marine Transportation, Precision Instruments, and Retail Trade posting the strongest gains. In contrast, 23 sectors declined, including Banks, Securities & Commodity Futures, and Metal Products.

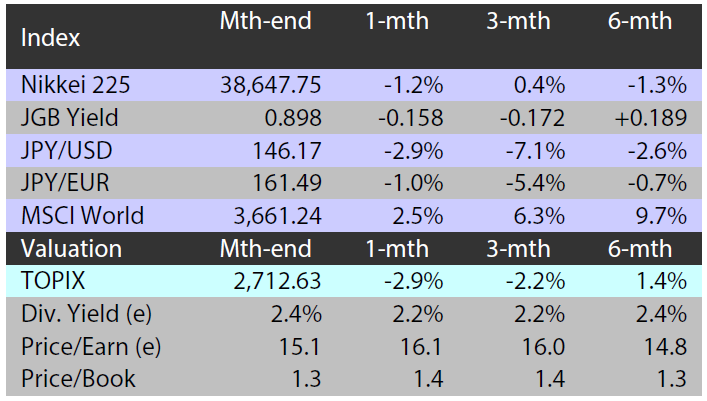

Exhibit 1: Major indices

Source: Bloomberg, 30 August 2024 |

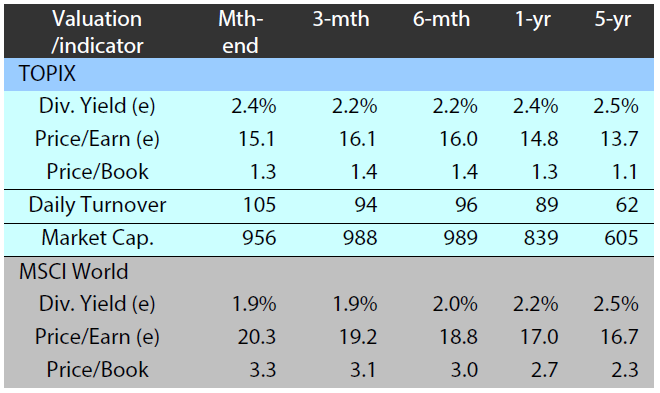

Exhibit 2: Valuation and indicators

Source: Bloomberg, 30 August 2024 |