Now that the Bank of Japan (BOJ) has exited its unconventional policy measures, particularly negative interest rates, the key question among global investors, especially those who remember Japan’s years of stop-start recovery attempts, is whether this time is really different. In other words, is there enough gas left in Japan’s tank? We believe the answer is yes, because Japan’s economic recovery is filtering through to household prosperity, underpinning the foundations of a structural recovery, rather than another flash-in-the-pan cyclical upturn.

Three compelling components to Japan’s domestic growth story are:

-

The pursuit of more “home-grown” investing

-

Retirement planning implications

-

Japan’s role as a “Magnificent Seven” diversifier

Japan’s pursuit of more “home-grown” investment

Households in Japan have historically been chronically underinvested in financial markets compared to global counterparts. However, while building up cash savings— even in a zero-interest rate environment—was rational in a deflationary economy, doing so amid even mild reflationary conditions is not. Reflation presents households with a clear monetary incentive to participate in financial markets and to seek returns at least capable of keeping up with the still-unfamiliar challenge of inflation. A reason to expect future income growth now provides a catalyst for behavioural change.

On this front, the new Nippon Individual Savings Account (NISA) regulations that took effect in 2024 are well-timed. Not only do NISA's tax incentives encourage the accumulation of long-term savings in financial market instruments, but they also provide incentives for market entry in the current year. They also prioritise long-term investing, opening the door to dollar cost averaging and to the exponential benefits of compounding investment returns over time, known in the West as “the eighth wonder of the world”.

Retirement planning implications

Now that the NISA system has been reworked, it seems likely that the next target for reform will be changes in the tax treatment of retirement vehicles, which would further encourage households to participate in financial markets. The “wealth effect” suggests that people tend to spend more as the value of their assets rise. When people see their investments growing or their home values rising, they feel more secure about their financial future. This increased confidence can lead them to spend more on goods and services. Therefore, real wage rises coupled with greater equity market participation could have a huge positive impact on Japanese households, and Japan’s economic growth in total. Even a small marginal change in domestic consumption and investments could have a meaningful impact on GDP overall.

Japan’s role as a “Magnificent Seven” diversifier

One of the most notable trends over the past couple of years has been the performance of the “Magnificent Seven” technology mega-caps in the US, with Apple, Microsoft, Nvidia, Tesla, Alphabet, Amazon and Meta buoyed by the potential for artificial intelligence (AI) to transform global industries. By contrast, Japan’s equity market progress really has been much more broad-based. And in terms of valuations, there’s little to suggest Japanese equities are overvalued.

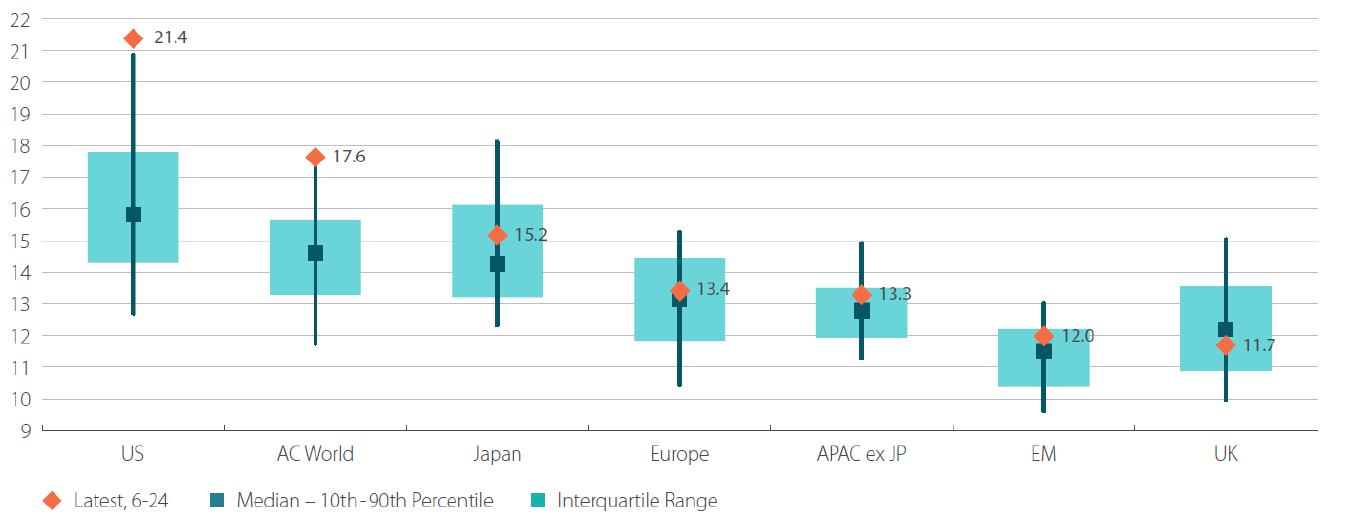

Valuations are not as stretched compared to historical valuations of US (and therefore world) stocks over the last 20 years. Indeed, looking at the US and the MSCI ACWI, Japanese forward price-to-earnings are still within their 20-year historical range. Any investors who feel valuations look stretched in the US may want to consider increasing their exposure to Japan, where more bargains are likely to be had, before the cycle starts to turn.

Chart 1: MSCI, Mid & Large Cap, 12m-forward P/E (data for the last 20 years)

Source: MSCI, Nikko AM Global Strategy & Macrobond. Data as of June 29, 2024.

Summary

The current conditions driving Japan’s normalisation are conducive to sustained secular out-performance in Japanese equities, given that the structural reforms taking place are of a long-term nature. For overseas investors who failed to participate fully in Japan’s equity market comeback in 2023, we would argue that it’s not too late and that the volatility in 2024 is providing a long-term opportunity to gain exposure to Japan’s rebirth.

To learn more about unlocking hidden value in Japan, download the Nikko AM investment guide here.

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.