Summary

- China has been feeling the pressure with Donald Trump due to return for his second term as US president. However, during Trump’s first term China actually outperformed the S&P 500 index, which demonstrates the importance of domestic policies over external pressure

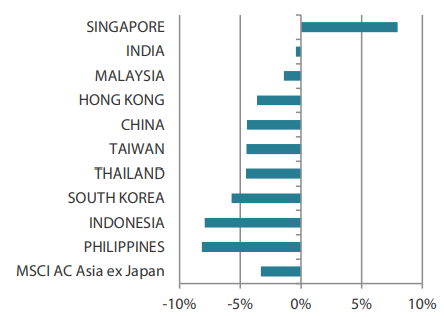

- Asian markets struggled for a second consecutive month, with the MSCI AC Asia ex Japan Index declining 3.3% in US dollar (USD) terms. China's latest stimulus measures underwhelmed, and the global markets digested the US presidential election results. The Philippines (-8.2%) and Indonesia (-7.9%) were the worst-performing markets while Singapore (+8.0%) was the only market that gained.

- Looking beyond the US elections, we continue to expect disinflation to continue in the US, accompanied by further interest rate cuts. Oil prices are expected to remain depressed while US dollar strength could peak due to high valuations. Elsewhere, China is pushing through counter-cyclical stimulus after its policy shift. These factors could create conditions for Asian markets to perform better. We remain focused on the bottom-up drivers of idiosyncratic stock returns, especially where positive fundamental changes improve the longer term sustainable returns of a company.

Market review

Asian markets retreat for the second straight month amid caution

The Asian markets drifted lower in November with the exception of Singapore. The MSCI Asia Ex Japan Index fell 3.3% in US dollar terms for the month. The region's biggest focal point remains on China's potential plans for bolder fiscal support, but Beijing's latest moves continued to lack more direct measures to boost consumer spending. Traders also spent much of the month weighing the economic outlook of a second Trump administration. Meanwhile, the US Federal Reserve (Fed) cut its key interest rate by a quarter-point in a widely-expected move. However, the Fed signalled that it may take its time easing policy going forward.

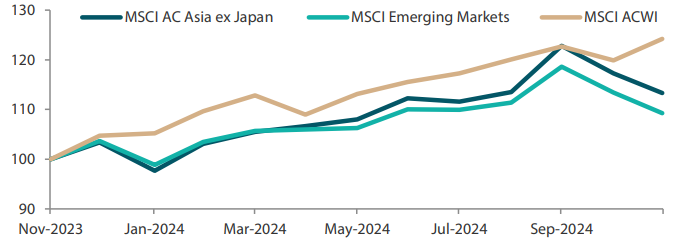

Chart 1: 1-yr market performance of MSCI AC Asia ex Japan vs. Emerging Markets vs. All Country World Index

Rescaled to 100 on November 2023.

Source: Bloomberg, 30 November 2024. Returns are in USD. Past performance is not necessarily indicative of future performance.

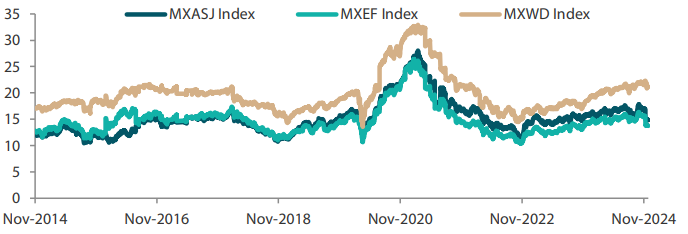

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

Source: Bloomberg, 30 November 2024. Returns are in USD. Past performance is not necessarily indicative of future performance.

Chinese stimulus package falls short of market expectations

In North Asia, Chinese stocks shed 4.4%. Chinese authorities unveiled a Chinese yuan (CNY) 10 trillion debt swap programme to help defuse local government debt risks, but they stopped short of unleashing new fiscal stimulus to promote growth. This fell short of market expectations, particularly in the face of president-elect Trump's threats of imposing additional tariffs on Chinese shipments. Meanwhile, data showed that China's inflation edged up 0.3% year-on-year (YoY) in October, while industrial output growth missed expectations and slowed to 5.3% YoY. However, consumers activity increased with retail sales surging 4.8% YoY, boosted by the annual Singles' Day sales festival. Hong Kong dipped 3.6%, but China's Vice Premier He Lifeng did pledge more support for Hong Kong's financial markets. This includes support for more high-quality Chinese companies to list in Hong Kong, improving mutual market access and issuing treasury bonds.

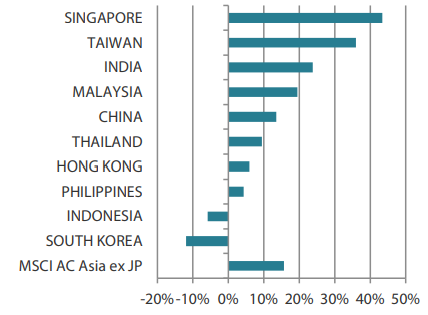

South Korea (-17.4%) remained the worst performer among major Asian markets in the year-to-date period, after shedding 5.7% in November amid growing trade and economic concerns following Trump's election victory. The Bank of Korea (BOK) trimmed its 2025 GDP growth forecast from 2.1% to 1.9%. The central bank also cut its benchmark interest rate by a quarter-percentage point to 3%, in an unexpected back-to-back easing following October's policy shift. In trade-dependent Taiwan (-4.5%), exports rose by a less-than-expected 8.4% in October, as demand for tech products driven by the artificial intelligence (AI) boom was outweighed by the sluggish economy of top trading partner China. Still, Taiwan adjusted its 2024 and 2025 economic growth forecast upwards to 4.27% and 3.29% respectively. However, Taiwan acknowledged that new US tariffs could curb growth in 2025.

Singapore's stock market having its moment in the sun

Performances within ASEAN markets were varied. Singapore (+8.0%) was not only the strongest index market by some margin in November, but it was also the best performer (+33.8%) in the year-to-date period. The city-state raised its growth forecast for 2024 to around 3.5%, as the economy is recovering faster than anticipated. Meanwhile, the Philippines (-8.2%) experienced the biggest decline in the index in November. The Philippine economy grew 5.2% YoY in the third quarter, its slowest annual pace in over a year as severe weather disrupted government project spending and dampened farm output. The central banks in Malaysia (-1.4%) and Indonesia (-7.9%) kept their benchmark interest rates unchanged at 3% and 6%, respectively. Thailand (-4.5%) also lagged the index. The Thai government is considering a series of fresh fiscal measures to sustain economic recovery, including the next phase of its cash handout stimulus programme scheduled for the second quarter of 2025.

Weaker corporate earnings weigh on Indian equities

Indian shares inched down 0.4%, as lacklustre corporate earnings results and stretched valuations continued to weigh on sentiment. Bribery charges against Indian conglomerate Adani Group also raised concerns of broader repercussions and cast fresh doubts about corporate governance in the country. Separately, India's October retail inflation rose 6.2% YoY, breaching the central bank's target range of 2–6% for the first time in over a year.

Chart 3: MSCI AC Asia ex Japan Index 1

For the month ending 30 November 2024

For the year ending 30 November 2024

Source: Bloomberg, 30 November 2024.

1

Note: Equity returns refer to MSCI indices quoted in USD. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Market Outlook

Focus remains on bottom-up drivers of idiosyncratic stock returns

As the dust settles following the US elections, the market has swiftly and efficiently discounted extreme scenarios under a Trump administration. After all, the market is significantly more prepared this time, and faster to extrapolate based on experiences from Trump's first presidential term. Yet, as we have seen throughout history, reality is often different from extreme election campaign proposals. If the policies of this new Trump administration prove to be less extreme, there could be significant reversal of the ongoing Trump trade. Notwithstanding the US elections, we continue to expect ongoing disinflation in the US, accompanied by further Fed rate cuts as the US labour market has eased considerably. Oil prices could remain depressed while US dollar strength could peak due to high valuations. China is also pushing through counter-cyclical stimulus after its policy shift. These conditions could favour Asian markets. Our focus remains on the bottom-up drivers of idiosyncratic stock returns, especially where positive fundamental changes lead to improvements a company's longer term sustainable returns.

Expect China to adopt more aggressive policy measures to counteract further US pressure

China, in particular, has been under pressure in the lead up to the US elections, as Trump floated extreme tariffs during his election campaign. However, we expect the Trump administration's approach to foreign policy to be a lot more transactional rather than ideological, as we have observed under current US President Joe Biden. Hence, eventual tariffs imposed by Trump's administration could potentially be significantly less severe compared to the proposals made during the election campaign. Valuations are also significantly lower compared to when Trump first became president. What could surprise many investors is that China actually outperformed the S&P 500 index during Trump's first term, which demonstrates the importance of domestic policies over external pressure. To this end, our view is that China's policy stance underwent a shift in September, as evidenced by the changes in messaging and top-down coordination. We expect more aggressive policy measures from China in the coming months in response to any moves by Trump.

Preference for semiconductor and communications-related names in Taiwan and South Korea

In the rest of North Asia, the incoming Trump administration could potentially support regional stability, as it may deter Taiwan from making hasty decisions that could jeopardise the status quo. Nevertheless, the South Korean and Taiwan markets have continued to diverge, in part due to changes in the tech sector. In Taiwan, AI-related demand continues to be the dominant driver of better earnings, despite increasing questions on the returns on investment this infrastructure roll-out may yield for hyperscalers.

In contrast, South Korea has lagged on the back of a weaker dynamic random-access memory (DRAM) market, delays in Samsung Electronics' high bandwidth memory business and disappointments in policymakers' Value Up efforts to boost capital markets. We remain selective, preferring semiconductor and communications-related names which have shown consistent adaptability towards new opportunities and are better prepared for the changing geopolitical landscape.

Recent valuation correction provides an opportunity to increase exposure in good quality Indian companies

The structural industrialisation trend in India and ASEAN, which is driven by the diversification of global supply chain away from China, is expected to continue and may even accelerate under a Trump administration. The bottom line remains that the US onshoring efforts are structurally constrained by availability and cost of labour. We expect wages and the growing middle class to be well supported as the region industrialise, driving a new wave of consumption across the region.

While the long-term investment narrative of the region is well understood, the expensive valuations of Indian companies have often been a point of contention for investors. In this regard, the recent moderation in the valuations of Indian companies, driven by short-term cyclical economic weakness, provides an opportunity for long-term investors to increase their exposure to good quality Indian companies with high sustainable returns. We remain committed to quality franchises in areas where we continue to believe fundamental change and sustainable returns are undervalued.

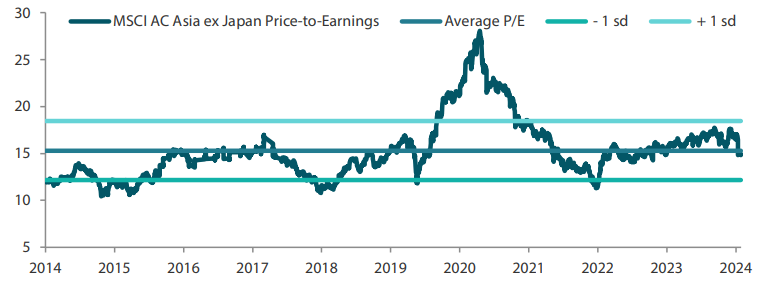

Chart 4: MSCI AC Asia ex Japan price-to-earnings

Source: Bloomberg, 30 November 2024. Ratios are computed in USD. The horizontal lines represent the average (the middle line) and one standard deviation on either side of this average for the period shown. Past performance is not necessarily indicative of future performance.

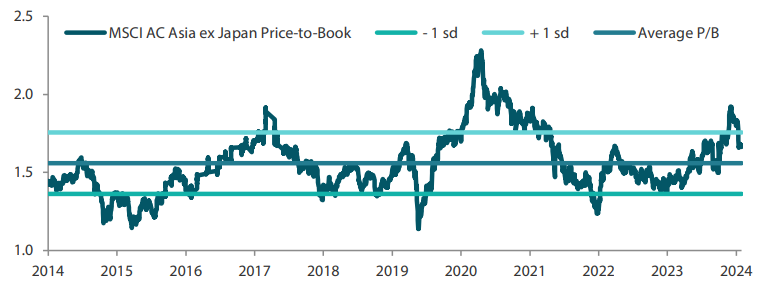

Chart 5: MSCI AC Asia ex Japan price-to-book

Source: Bloomberg, 30 November 2024. Ratios are computed in USD. The horizontal lines represent the average (the middle line) and one standard deviation on either side of this average for the period shown. Past performance is not necessarily indicative of future performance.